InPost (INPST) Investment Thesis

InPost is an advantaged parcel delivery company that is taking market share in Europe, deploying capital at extremely high returns on incremental capital, and offers an asymmetric return probability.

Summary: InPost is a competitively advantaged parcel delivery company that is taking market share against traditional logistics competitors via its last-mile network of automated lockers. InPost’s services dramatically reduce the total cost of package delivery and is a rare win-win for all participants in its ecosystem. InPost operates as the low-cost operator in Poland, yet simultaneously has the most profitable business model. Despite a competitive industry, InPost has firmly established themselves as the market leader with a multitude of advantages – primarily stemming from economies of scale. Competition has been unable to dent InPost’s market share despite absurd price cuts and they seem unlikely to do so in the future. InPost has a long runway for continued reinvestment of internal cash flows at unusually high returns on incremental capital. The range of future outcomes for the business and its share price is asymmetrically skewed towards the positive.

Overview

InPost is a logistics company that provides parcel delivery services in Europe. Its primary base of operations is in Poland, where 60% of its revenues and 90% of its profits are generated.

Founded in 2006, InPost is a relatively new entrant to the world of parcel delivery when compared to its traditional competitors, each of which have 50+ year histories. Despite this, InPost has been successful in taking market share in its home market of Poland and is replicating its strategy methodically across Western Europe, most notably in France and the UK. The key difference between InPost and these legacy delivery services is that InPost has popularized the out-of-home delivery method. Practically, this means that InPost delivers the majority of its parcels to lockers, rather than to doorsteps.

InPost has built a network of more than 20,000 locker machines, known as Automated Parcel Machines (APMs), in Poland. On average, there are ~150 individual locker containers per APM, yielding more than 3 million locker containers in Poland. These APMs are conveniently located on sidewalks, streetcorners, train depots, and parking lots outside of convenience and grocery stores, apartment buildings and the like. APMs are almost always outdoors and thus available 24/7. Customers simply step up to the machine, scan the QR code and collect their packages.

If you were to walk around a city in Poland you would easily find that InPost’s APMs are all over the place. Today over 60% of the population lives within a 7 minute walk of an APM. That number increases to 85% when you consider only the urban residents. There are competitors, to be sure, but InPost drowns out the competition with more than 64% market share of the APM locations and 85% of the lockers available in the country.

Let’s pause for a moment. The cynic inside of me has something to say… why would a customer willingly choose to have their package delivered to a locker rather than their doorstep in the first place? That seems inconvenient. Moreover, why should this company enjoy any sort of competitive advantage? It’s just a locker machine after all. Competitors should be able to locate a locker right next to them and this should eat into InPost’s volumes, right? How could there be any barriers to entry or pricing power whatsoever?

Hear me out.

First question. Why would a customer willingly choose to have their package delivered to a locker? Answer: Because it is dramatically cheaper.

If you have ever studied the e-commerce industry then you will know that last-mile delivery is by far the most expensive part of the fulfillment chain. Last-mile accounts for ~50% of the total cost to deliver an item. A parcel delivery person can only deliver ~150 packages per day to doorsteps on average. That is a fixed number that never changes. Yet, with InPost’s network of APMs, a parcel delivery person can now deliver those same ~150 packages in a single trip.

This dramatically reduces the total cost of last-mile delivery by as much as 80-90%. It also increases the effectiveness of postal delivery workers and allows InPost to gain leverage over their primary fixed expenses – labor and fuel.

Looking at each of the participants in the value chain:

Consumers get significantly cheaper prices on items via the reduction in delivery costs, control over pickup times, and fast delivery (95% of parcels are delivered within one day of purchase).

Online merchants who partner with InPost (of which there are >50,000) benefit from the aforementioned total cost reductions and get higher conversion rates.

APM Location landlords get increased rental revenue for the square footage that they already own and, importantly, increased foot traffic for the stores that are located there.

And InPost, the facilitator of all of this, gets to occupy the single-most valuable position within the entire value chain. They not only create meaningful value for all participants that is superior to the historical modus operandi, but they also get to capture a significant percentage of those economics for themselves as well. It is revealing that InPost is 8-10x cheaper than its traditional competitors yet it also captures higher EBITDA margins (48% in Poland, 32% consolidated) than their competitors’ gross margins (which range from 17-26%).

Second question. Why should this company enjoy any sort of competitive advantage?

InPost’s competitive advantages almost all stem from their core advantage of scale and reliability. As mentioned earlier, InPost has more than 20,000 APMs located within a 7-minute walk of 85% of the urban population in Poland. But it would be a mistake to describe InPost as merely an owner of these lockers and little more. InPost owns all of the back-end infrastructure required to facilitate parcel delivery, including the central distribution center, regional hubs, and hundreds of delivery depots. Additionally, they have integrated with more than 50,000 online merchants and when a consumer selects the delivery method, they overwhelmingly select InPost as their preferred option. Competitors, in order to compete with InPost in APMs, must not merely install lockers in convenient locations (costing upwards of $400 million USD). They must also invest heavily in back-end logistics and integrate with tens of thousands of online merchants. But that’s not all. Consumers must willingly select the competing solution over InPost, a company that they know and use extremely frequently. 1

Up to this point, I have mainly referred to “competition” as being the sort of merchant-agnostic pure-play delivery company (DHL, UPS, FedEx, etc.). But there is a second form of competition that exists in the form of marketplaces (Amazon, Allegro, etc). These companies already have parcel volumes running through their own marketplace operations and they can funnel customers to their own APMs, should they choose to do so. Early in my research process, I viewed this as an enormous competitive threat, given that Allegro currently accounts for 17% of InPost’s total revenues. In 2020, InPost signed a 7-year deal with Allegro and said that in 2022 they would adjust the price in accordance with inflation. That adjustment ended up being 12% and Allegro was obviously unhappy with it. A number of Allegro shareholders pushed Allegro to build out their own APM network as a result of this cost increase and CEO, François Nuyts, obliged by deploying capital expenditures into building out 2,500 APMs in Poland costing between $50-100 million USD. His intention was to build out thousands more until he resigned for “personal reasons”. In his stead arrived Roy Perticucci, the former head of European operations and fulfillment at Amazon. Seemingly a perfect hire for building out a larger APM network. However, Ray performed an about-face in this regard. On his first earnings call with investors he said this:

“This is, I think, the second year or the third year that we've been working with these [last-mile] capabilities. And I think it's always respectful of the challenge to make sure that you're all buttoned up before you make another major jump. And question for me is, we've built a successful business on being asset-light. And so developing our own capabilities about choices, about speed, reliability and cost. As long as we have good choices from the market, that will also affect our speed or lack thereof in terms of further developing our own… Historically, we've been an asset-light model. And I think wherever we can that's where we want to stay. So as long as we can work with our carriers, I don't have a huge priority to rapidly grow out the market”

On his second earnings call since taking the helm, three months later, he added this:

“And I think, particularly in the final mile, particularly in lockers. This is a place where we want to be a lot more conservative in terms of future investments.”

In an effort to remain asset-light, Roy Perticucci realized that this was a loss-making project that was going to cost 4-5 years’ worth of cash from operations to build out, and that they had other, more pressing priorities to focus on, especially considering that there is a substantial amount of debt on the balance sheet and an intense competition for market share with Amazon.

Ultimately Allegro could one day come back to this project and continue to add to its last-mile APM network. This represents a legitimate risk, but not an existential one to InPost. The fact remains that InPost is agnostic and is capable of accepting orders from all merchants, including Allegro. Allegro’s fulfillment network will only facilitate orders from its existing network which is not a sufficient amount of volume at this time (or in the near future) to justify a high enough utilization rate on these APMs to earn an acceptable return on that investment. InPost remains the partner-of-choice for the time being because of its ability to provide reliable, rapid fulfillment at the lowest total cost in Poland.

A similar event is occurring in the UK where Amazon is actually reducing its APMs while InPost is aggressively expanding.

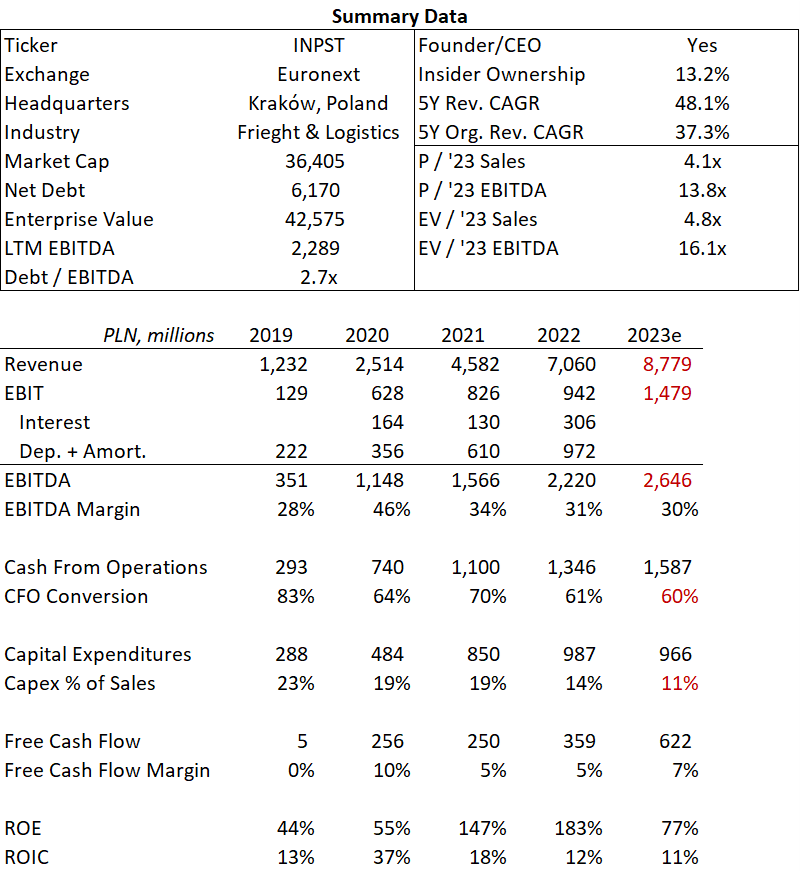

In sum – InPost is the most dominant parcel delivery company in Poland. Its network of >20,000 APMs reaches the vast majority of the Polish population and facilitated 550 million parcels in the last twelve months. This produced PLN 4.7 billion revenue (~$1.1 billion USD), which accounts for 60% of total sales. EBITDA margins were 48% and grew 28% y/y. There remains a significant source of revenue growth here because Polish e-commerce remains deeply underpenetrated at ~15% relative to European peers. The Polish APM network is approaching a saturation point and increased revenue in Poland will flow through existing APMs, thereby driving asset turns and profit margins.

International Expansion - France

In 2021, InPost acquired Mondial Relay, a France-based international package delivery company that was founded in 1997. InPost paid PLN 2.4 billion ($550 million USD) for ~1x revenues and ~7x EBITDA for France’s second largest courier service. One of the most important assets that Mondial Relay brought to the table (in addition to volume) was more than 17,000 pick-up-drop-off (PUDO) locations. PUDO locations are basically a simple partnership with a local convenience store or retailer in which the courier drops off packages with the retailer and then the customers come to collect their items from the store. This was a fairly popular choice among French consumers because the aforementioned convenience and cost savings of OOH delivery still apply with the PUDO model. A customer would walk into the store, wait in the checkout line, scan their QR code, collect their package, and then be on their way.

Retailers like this approach because it drives foot traffic into their stores and increases the likelihood that the customer will purchase something while they visit. Mondial Relay’s management team was effective in noticing the savings to be gained by this approach and leaned heavily on this as a growth strategy.

InPost, seeing the opportunity to crank this business model one step further, acquired Mondial Relay and immediately went to work leveraging these pre-existing relationships with retailers to quickly install APM locker machines outside of these retail stores. Merchants generally liked the addition of an APM even more than the previous PUDO model because it still drove foot traffic to their store, but it also reduced the need for the retailer to have to store those items until a customer came to collect them. Further, it eliminated the number of non-customers who were just standing in line to collect their packages and freed up employees from having to go to a back-room to collect the item for the individual.

InPost retained the Mondial Relay brand and installed more than 1,000 APMs within the first twelve months of ownership. Today, 24 months post-acquisition, there are more than 4,000 APMs, largely installed within the best locations of the pre-existing PUDO network.

France, like Poland, is similarly underpenetrated in e-commerce at only 11%, yet the market is currently more than double that of Poland at $60 billion USD with no focused APM company in existence.

France is similar to Poland because the OOH delivery option is already well established. Yet none of the five logistics brands in the country have invested in an APM network because they either do not believe that it will work or are unwilling to pay the upfront capital expenditures to get the ball rolling. Due to this, there is currently a massive opportunity for InPost to replicate their Polish blueprint for success in France with a distinct advantage that they did not have in previous years in Poland… the pre-existing PUDO locations which they can quickly convert with a value-additive proposition. In the immediate term, France (and the UK) are the top two priorities from a capital expense perspective, but in the medium- to long-term there is a natural extension of this strategy to the other countries that Mondial Relay has an established presence in.

In the 24 months post-acquisition, InPost has grown Mondial Relay’s revenues by 23% to PLN 2.9 billion, while EBITDA has shrunk by 6% (to an 11% margin) while the company continues to invest heavily in expanding their network capacity. A key reason for this lack of profit growth is because Mondial Relay is in growth-now mode and it would be counter-intuitive for them to pass through increased fuel and labor inflation costs to the merchants that they are attempting to aggressively gain market share with.

International Expansion – United Kingdom

InPost has been operating in the UK for the last decade with minimal success until recently. The UK is unique compared to other European countries in more ways than we could list here. But of the notable reasons, e-commerce is well established (29% penetration rates) and consumers are widely accustomed to receiving packages at their doorstep. The cost-savings for OOH delivery are constant geographically, but it has been a challenge to build against a developed habit, whereas in Poland and France, customers have “grown up” in e-commerce with OOH delivery.

InPost remains committed to their bread-and-butter approach to facilitating online B2C orders, but they have narrowed their focus more specifically in recent years to online fashion retailers and peer-to-peer marketplaces. The UK is one of the most developed markets in the world for online fashion retailing. Online fashion retailers such as Sainsburys, Next, Asos, John Lewis, Marks & Spencer, and Zara produced a combined $14 billion in revenue in 2022. Yet a common problem for these e-retailers is that the average return rate of online apparel orders is 25%, an astronomic rate that is a large cost burden for these companies.

In 2021, InPost approached dozens of these fashion retailers with a labelless return proposition, that required only that the customer place the item in the locker and scan the QR code. The cost-savings that e-retailers gained from this approach could immediately be felt on bottom-line profit margins. It also increased convenience for customers… which is always a winning proposition.

In addition to being a hyper-competitive industry with frequently slim (and often times non-existent) profit margins, fashion retailers have faced significant inflationary pressures in the last two years. This has only accelerated the degree to which these companies have relied upon InPost to facilitate both returns and orders. InPost is prioritized at checkout with these partners and has seen a rapid increase in their share of checkout.

InPost has finally turned the corner and established proof-of-concept in the UK, and is investing heavily in APM roll-out in response to increasing demand for their services. Despite it being in the early stages of the growth cycle, InPost is already the largest agnostic APM provider in the country, with over 5,400 APMs within a 7-minute walk of urban residents in “core” cities.2

Amazon is the largest APM provider in the country, and rightly so given their dominant market share of e-commerce in the country. Yet they are not merchant-agnostic and unlikely to ever perform fulfillment for rival merchants (eBay, Vinted, Sainsburys, etc.). That leaves a near-unlimited white space for InPost to expand in the UK unabated with little competition while merchants are finally realizing the cost benefits of the OOH delivery method and evangelizing the method on behalf of InPost to their own customers.

A potent combination of deep cost savings and maximal convenience is core to the InPost value proposition, and it is beginning to be recognized more broadly by the UK population. One UK-based full-time eBay seller posted a video a year ago describing the convenience of the InPost lockers and mentioned that he filled up the entire bay of lockers at one APM location with shipments to his customers the day before, and that he was returning the next day to do it again.

Which brings us to 2023. In July InPost announced that it had acquired a 30% stake in Menzies with a three-year option to acquire the remaining 70% stake. Like Mondial Relay, Menzies is a parcel delivery company, yet without the brand-recognition as an OOH delivery company. Therefore InPost will be retaining their brand as they seek to continue to grow UK market share. What Menzies brings to the table is a nation-wide infrastructure to support the fulfillment of this increased demand and the addition of incremental APMs.

InPost had previously partnered with Hermes UK, another parcel delivery company, but the lack of ownership led to a lack of control over delivery priorities, route optimizations to APMs, and the like. On Stream, an expert network database, there is a conversation with the Former Network Head of InPost UK, where he outlined this problem and walked through the logic of this Menzies acquisition way back in February of 2022: 3

Customer trust is one of the key elements into getting into profitability and also focusing in on services that have a higher profit margin like returns and label-less returns, etc. There's high profitability in those areas. By focusing in on those areas, you can definitely capitalize. I would also say couriers. If you were able to take the courier service in-house, that would definitely accelerate towards profitability. You have less cost, etc. It's all managed in-house. You also have more control over the trust in your network.

My personal opinion is, with a courier like Hermes, you are very limited in the service that you can provide for your customers due to Hermes is on-time delivery. If you really want a challenge in this day and age, you have to have a stronger on-time delivery. Hermes is a very big ship. To turn that ship around is going to potentially take too long to get to where you need to be, in my opinion, as a business in delivery today in this day and age to be reliable and to be on time. My personal view is that they have to do that at some point soon.

Menzies brings the logistical backbone that was previously lacking, and which is a key source of competitive advantage to their Polish and French operations. This new logistics capability is allowing InPost to facilitate faster, more reliable delivery of their B2C, C2C and labelless returns orders. But it is also allowing InPost to funnel portions of Menzies’ existing volume through its APM network, thus driving higher APM utilization and higher profit margins per order.

As the former UK Network Head predicted, this is having an effect on profit margins. InPost’s UK business is closing the gap rapidly on profitability, with 1H’23 producing a -10% EBITDA margin, up from -22% in the year-prior. By the end of this year, InPost is guiding for break-even EBITDA margins. 4

Financial Notes

InPost’s valuation is underpinned by its profitable unit economics. APM operating cash-on-cash payback period is ~14 months and the rate of return is in excess of 60% in Poland. As the APM market in France and the UK increases in their maturity, similar payback periods can be expected.

InPost is leveraged, with PLN 6.2 billion of net-debt, for a leverage ratio of 2.7x EBITDA. 93% of this debt is due between 2025 and 2027, and it should be covered by the Poland segment’s cash flows from operations.

InPost is also characterized as one of decreasing capital intensity. InPost depreciates each APM on a 10-year basis, yet these machines’ useful lives are estimated to be in excess of 20 years. There has been and will continue to be a decrease in growth capital expenditures as a percent of revenue (20% in 2021, 16% in 2022, and 11% in 1H’23), and InPost management has committed to spending no more than PLN 1.2 billion of capital expenditures per year for the foreseeable future (presumably 1-3 years). The majority of this capex will be going towards France and the UK.

Valuation – (Condensed Thoughts)

I believe that InPost’s Polish operations account for approximately all of InPost’s market valuation, thereby leaving the remainder of the international assets, revenues and profits available for free. Using a simplistic discounted cash flow model below, I estimate Polish revenue growth (itself a product of parcel volume growth and price increases) to continue at a 5-year annual rate of 18%. I estimate no further increases in EBITDA although the company has guided higher. The key to their free cash flow profits will be in the increased conversion of free cash flow as a percent of EBITDA. This is going to ramp up significantly in the coming years because the management team has guided a near-total shift in capital expenditures away from Poland towards France and the UK in the coming years. This is due to Poland reaching a saturation point, coupled with the white space opportunity to replicate their business success in these countries.

Despite being valued at effectively nothing, neither of InPost’s international businesses are draining cash. France is minimally profitable with 11.6% EBITDA margins that are likely to expand in the coming years towards the 48% EBITDA margins that Poland produces today. Meanwhile, the UK business is expected to reach EBITDA break-even in Q4’23. These businesses are not worth nothing.

InPost’s Polish operations offer a cash cow for which capital might be redeployed at similar >30% returns on incremental capital. These incremental cash investments in addition to the existing international assets (which comprise 40% of revenues and 10% of LTM profits) are valued at effectively nothing. This offers the shareholder an asymmetric upside return likelihood with a seemingly high floor, that is underpinned by InPost’s Polish operations which will continue to grow at or above the rate of e-commerce in the country given their dominant position in the market coupled with seemingly sustainable competitive advantages.

Disclosure: Clients of Asheville Capital Management owns shares in InPost. Ownership is subject to change. These are not recommendations. The information contained in this document is compiled based on publicly available information and believed to be accurate. It is not intended to be financial advice. Please conduct your own due diligence.

Jake Barfield is the founder of Asheville Capital Management, LLC. Asheville Capital focuses on investing in a concentrated basket of world-class businesses before they are broadly appreciated as such.

Jake can be reached at jake@ashevillecapitalmanagement.com.

Over 90% of InPost’s volumes in Poland come from Heavy and Super Heavy users, defined as users who receive between 13-39 packages, and 40+ packages per year through the InPost network, respectively. These extremely sticky users make up ~25% of the Polish population.

Core cities being those with populations over 175,000.

https://stream.alpha-sense.com?docid=EC-020822-97686&utm_source=alphasense%20platform&utm_medium=document%20share&utm_content=EC-020822-97686&utm_campaign=1695830959211

“EBITDA” is misused by so many companies as an inflated non-gaap metric for profitability, but in InPost’s case it is actually the perfect metric because there is so much accelerated depreciation on the income statement from capital expenditures and because there is interest from the debt load that is gradually being paid down. Further, InPost is not using EBITDA as a tool to hide excessive stock-based compensation, which averages <1% of revenue and is treated as the cash expense that it actually is. Shares outstanding have remained unchanged at 500 million for 2.5 years.

I recently began looking into InPost, and this is by far the best write-up I’ve come across on the company. We had a similar service in Ireland called Parcel Motel, which eventually went out of business. It was initially popular because it allowed customers in Ireland to purchase items from the UK using a virtual address, which gave access to products that weren’t otherwise available. Brexit closed that loophole, and the work-from-home movement post-COVID was the final nail in its coffin.

Having seen the downfall of this service, I’m naturally more skeptical of InPost. I understand my perspective is quite unique, given that Ireland is different from the rest of Europe in terms of size and population density. I’m wondering if you could share why InPost might succeed where Parcel Motel failed?

Fantastic deep dive. I am based in Czechia and there's a local version of Inpost, Packeta Group (privately owned). Mix of PUDO and APM network (started as PUDO, then built up their APM network). Almost the same trajectory as Inpost in Poland - massive increase in revenues and profits over the course of its existence. Similar if not higher EBITDA margins. It's surreal because in Poland and Czechia you see the APM boxes everywhere, and everybody uses them. In big cities there are often locations where you see 5 of them next to one another, as there's intense competition. Then you go to Western Europe where the APM concept is still in its infancy. These 2 countries show that this model can be replicated everywhere else - just a matter of time before people realize the convenience of the box as opposed to a postman missing them at home at a specific hour and then dropping off the package at an undesirable location or returning back to sender. In Czechia, Packeta has also cleverly mixed the best of both worlds, enabling P2P package shipping between individuals - you ship via a PUDO joint that prints the shipping details on your package, and then the counterparty can collect via PUDO/APM (their choice). I am sure Inpost will figure this out too.